Introduction

If your savings account is earning almost no interest, you are not alone. Millions of Americans still keep their money in traditional savings accounts that barely grow over time. With inflation continuing to affect groceries, rent, insurance, and daily expenses, many people are now searching for smarter and safer ways to make their savings work harder.

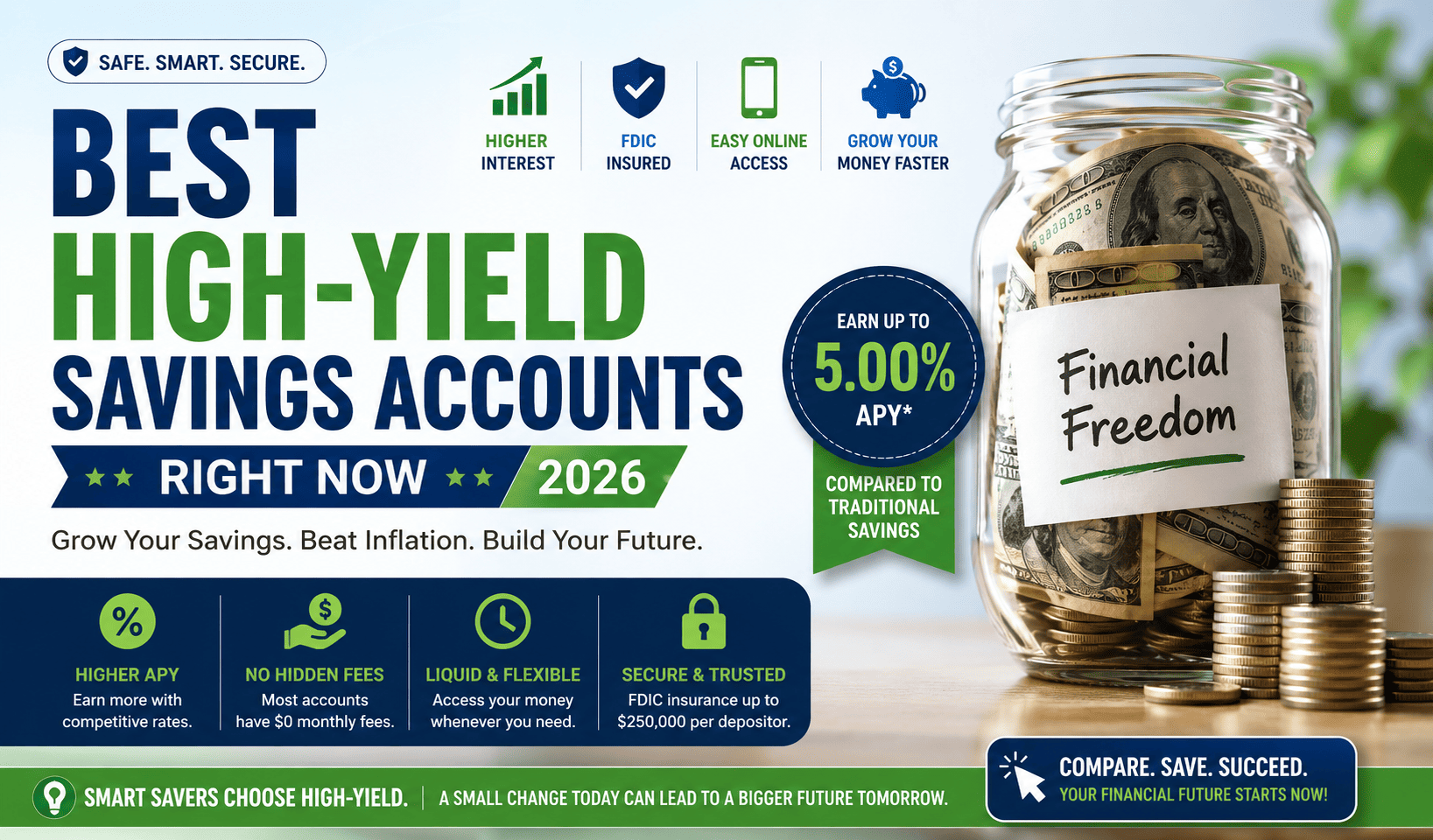

That is why high-yield savings accounts have become one of the most popular financial tools in the USA. They offer significantly higher interest rates compared to regular bank accounts while keeping your money accessible and relatively safe.

Whether you are building an emergency fund, saving for a home, or simply trying to beat inflation, choosing the best high-yield savings account right now could help you grow your money faster in 2026.

Quick Answer

The best high-yield savings accounts right now are typically offered by online banks and credit unions that provide higher APYs (Annual Percentage Yields), low fees, FDIC insurance, and easy digital banking access. Many top accounts in 2026 offer rates significantly higher than traditional savings accounts, making them a smart option for emergency funds and short-term savings goals.

What Is a High-Yield Savings Account?

A high-yield savings account is a savings account that pays a much higher interest rate than a traditional savings account.

Traditional banks often offer very low APYs, while many online banks provide much more competitive rates because they have lower operating costs.

For example:

- Traditional savings account: Around 0.01%–0.10% APY

- High-yield savings account: Often 3%–5%+ APY depending on market conditions

This means your money can grow faster while still remaining accessible for emergencies or short-term goals.

Most high-yield savings accounts in the USA are FDIC-insured up to applicable limits, helping protect your deposits.

Benefits & Key Indicators of the Best High-Yield Savings Accounts

Beginner-Friendly Features

- Higher interest earnings

- Easy online access

- Low or no monthly fees

- FDIC insurance protection

- Automatic savings tools

- Mobile banking apps

- No minimum balance requirements

Advanced Features

- Competitive APY rates

- Fast transfers

- Goal-based savings tools

- Linked checking accounts

- Daily compound interest

- Joint account options

Warning Signs to Avoid

- Hidden maintenance fees

- Very high minimum balance requirements

- Poor customer support

- Withdrawal restrictions

- Promotional rates that expire quickly

Causes, Financial Risks & Common Mistakes

Many Americans lose money simply because they leave cash sitting in low-interest accounts while inflation reduces purchasing power over time.

Common Financial Mistakes

Keeping Too Much Money in Checking Accounts

Checking accounts usually offer little or no interest, meaning your money is not growing.

Ignoring Inflation

Inflation can slowly reduce the real value of your savings if interest rates are too low.

Chasing Risky Investments for Short-Term Savings

Some people invest emergency savings into risky stocks or crypto assets, which may lead to losses when money is needed urgently.

Not Comparing APYs

Many consumers stay with traditional banks without realizing better options exist elsewhere.

Falling for Banking Scams

Fake financial apps and phishing scams are becoming more common in the USA. Always use trusted FDIC-insured institutions.

High-Yield Savings Account vs Traditional Savings Account

| Feature | High-Yield Savings Account | Traditional Savings Account |

|---|---|---|

| Interest Rate | Much Higher APY | Very Low APY |

| Online Access | Usually Strong | Varies |

| Monthly Fees | Often None | Sometimes Charged |

| FDIC Insurance | Usually Yes | Yes |

| Minimum Balance | Often Low | Sometimes Higher |

| Best For | Emergency Funds & Savings Growth | Basic Banking |

Best Financial Strategies for Using High-Yield Savings Accounts

Build an Emergency Fund

Financial experts often recommend saving at least 3–6 months of living expenses.

A high-yield savings account can help emergency savings grow while remaining accessible.

Automate Monthly Savings

Set up automatic transfers from your paycheck or checking account into savings.

Consistency matters more than large deposits.

Separate Savings Goals

Create different savings buckets for:

- Emergency fund

- Vacation

- Home down payment

- Car repairs

- Medical expenses

Combine Budgeting With High-Yield Savings

Popular budgeting strategies include:

50/30/20 Rule

- 50% Needs

- 30% Wants

- 20% Savings & Debt Payments

Pay Yourself First

Move savings automatically before spending on non-essential expenses.

Avoid Unnecessary Debt

High-interest credit card debt can quickly cancel out savings growth.

Prioritize paying down expensive debt while building savings steadily.

Money-Saving & Lifestyle Tips

Daily Habits That Help Savings Grow

- Reduce impulse spending

- Cancel unused subscriptions

- Use cashback apps carefully

- Meal prep at home

- Compare insurance rates annually

- Track monthly expenses

Financial Mistakes to Avoid

- Keeping all savings in cash

- Ignoring emergency savings

- Overspending on lifestyle inflation

- Using savings for unnecessary purchases

- Delaying retirement planning

Smart Wealth-Building Habits

- Save consistently

- Invest long term

- Improve financial literacy

- Avoid emotional spending

- Review financial goals regularly

Cost-Saving Strategies for Americans

- Shop warehouse stores

- Use high-yield savings for short-term goals

- Refinance high-interest debt if appropriate

- Compare utility providers

- Negotiate recurring bills

When to Seek Professional Financial Advice

While high-yield savings accounts are relatively simple financial tools, some situations may require professional guidance.

Consider consulting a certified financial professional if you:

- Struggle with serious debt

- Face loan defaults

- Need retirement planning help

- Experience major investment losses

- Need estate planning assistance

- Are unsure how to balance saving and investing

Professional advice may help create a more personalized financial strategy.

Who Should Care About High-Yield Savings Accounts?

1. Students

Useful for emergency savings and tuition planning.

2. Families

Helpful for managing household emergency funds and future expenses.

3. Seniors

Can provide safer cash growth compared to riskier investments.

4. Office Workers

Ideal for payroll savings automation and financial stability.

5. Freelancers & Gig Workers

Useful for handling irregular income and tax savings.

6. Beginners

Easy starting point for building better financial habits.

7. Small Business Owners

Helpful for short-term business reserves and operating cash.

FAQs

1. What is considered a good high-yield savings account rate in 2026?

A competitive high-yield savings account rate is generally much higher than traditional savings account rates and may vary depending on market conditions and Federal Reserve interest rates.

2. Are high-yield savings accounts safe?

Most high-yield savings accounts offered by FDIC-insured banks are considered relatively safe for storing cash within applicable insurance limits.

3. Can I lose money in a high-yield savings account?

You generally do not lose money due to market fluctuations like stocks, but inflation may reduce purchasing power over time.

4. How often do savings account interest rates change?

Banks may adjust APYs based on economic conditions and Federal Reserve policy changes.

5. Should I keep all my money in a high-yield savings account?

Not necessarily. Emergency funds and short-term savings often fit well in these accounts, while long-term investing goals may require different strategies.

Conclusion

Choosing the best high-yield savings account right now can be one of the smartest financial decisions for Americans looking to grow their money safely in 2026.

These accounts offer better interest rates, low fees, and flexible access compared to traditional savings accounts. Whether you are building an emergency fund, saving for future goals, or trying to stay ahead of inflation, a high-yield savings account can help strengthen your financial foundation.

Start by comparing trusted FDIC-insured banks, reviewing APYs carefully, and creating a consistent savings plan that fits your financial goals.