Introduction

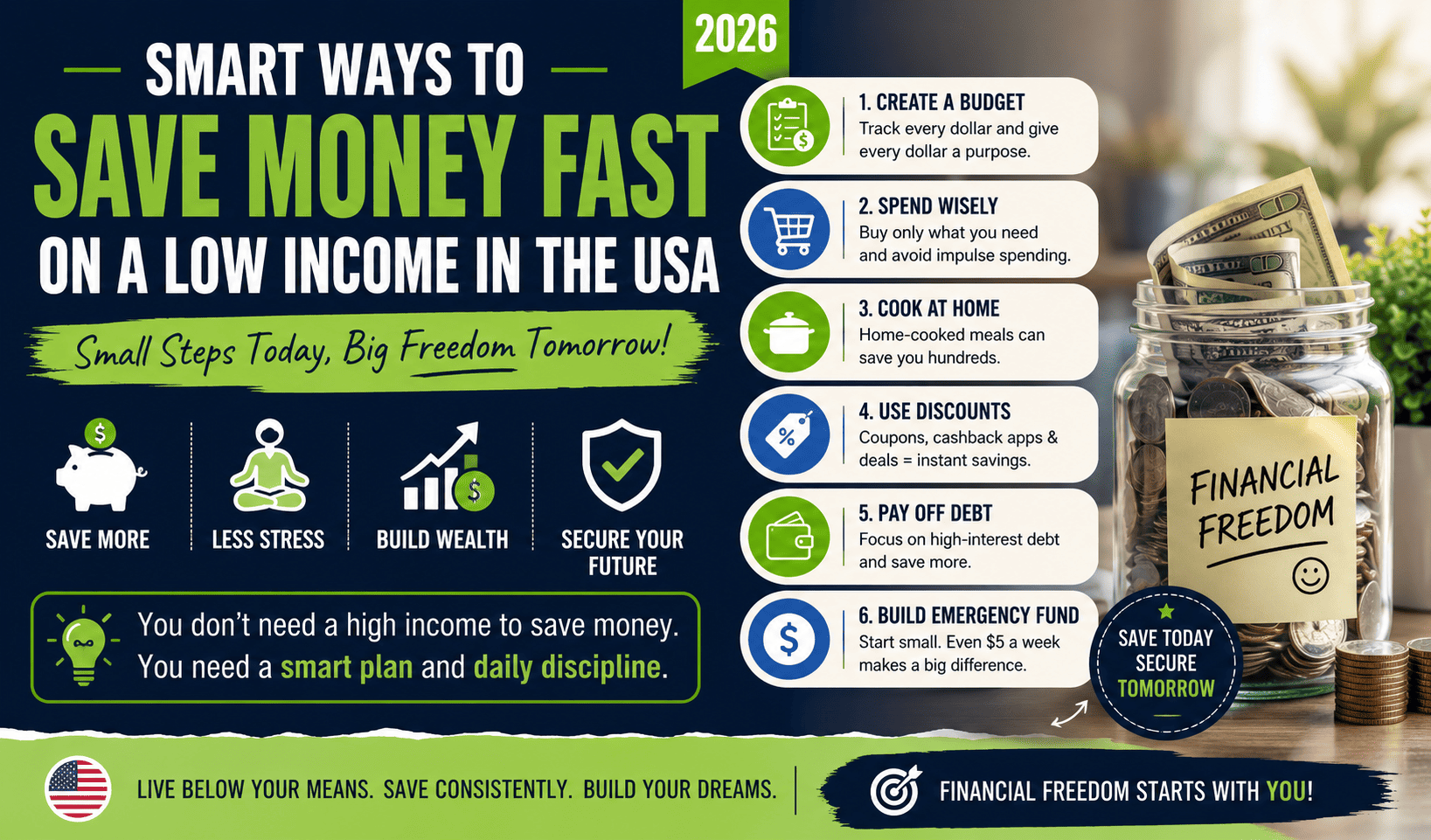

If you feel like your paycheck disappears before the end of the month, you are not alone. Millions of Americans struggle with rising living costs, credit card debt, unexpected bills, and poor savings habits. According to recent financial surveys, many households in the USA live paycheck to paycheck, making budgeting more important than ever.

The good news is that learning the right budgeting method can help you control spending, reduce financial stress, and build long-term financial stability. Even beginners can start improving their finances with simple and practical budgeting strategies.

Quick Answer: What Is the Best Budgeting Method for Beginners?

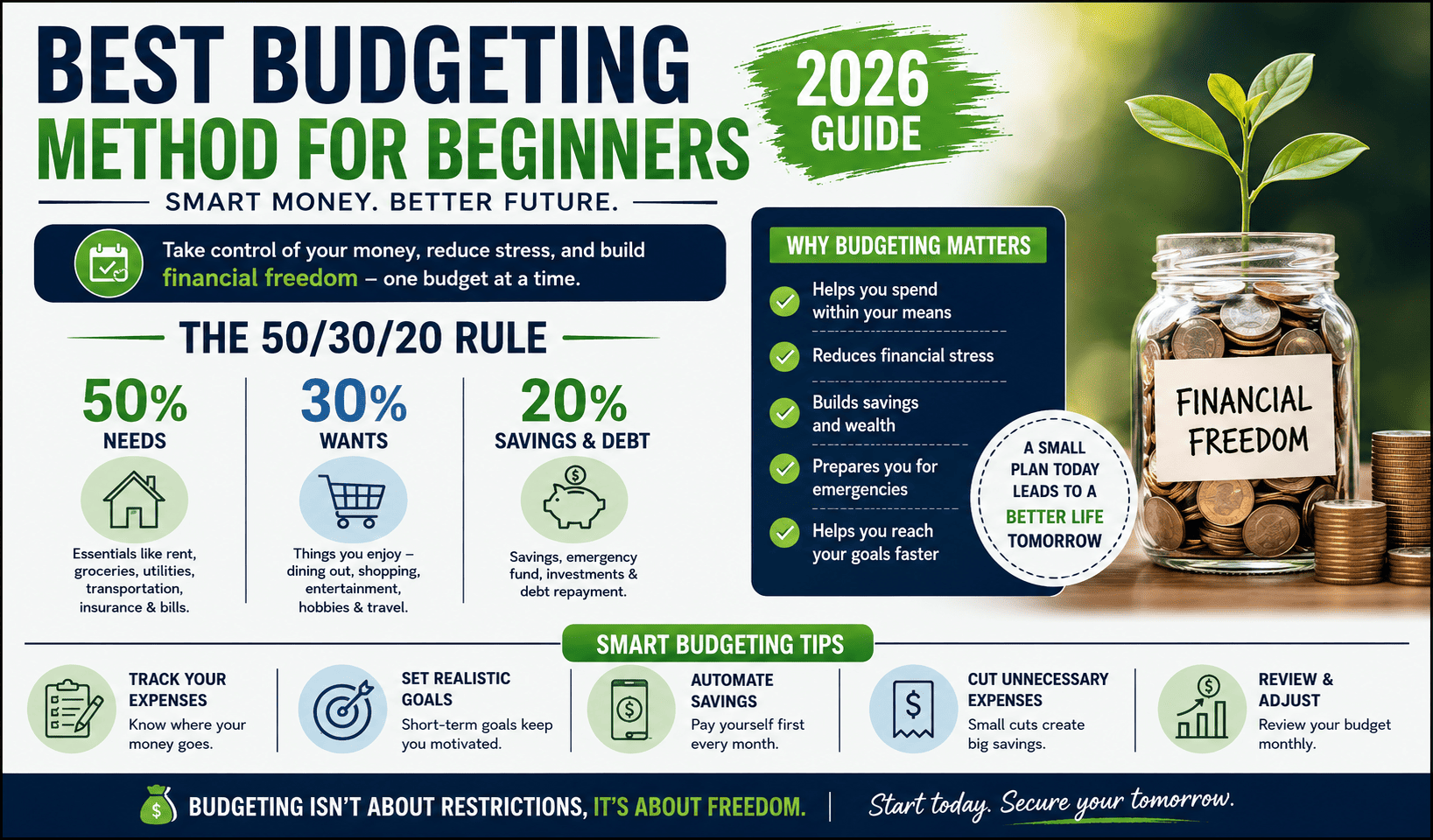

The best budgeting method for beginners is usually the 50/30/20 budgeting rule because it is simple, flexible, and easy to follow. It divides after-tax income into three categories: 50% for needs, 30% for wants, and 20% for savings and debt repayment. This method helps Americans manage money without feeling overwhelmed.

What Is the Best Budgeting Method for Beginners?

A budgeting method is a system that helps people organize income, spending, savings, and financial goals. The best budgeting method for beginners should be easy to understand, realistic, and flexible enough for daily life.

Many Americans fail at budgeting because they create complicated plans that are difficult to maintain. Beginner-friendly budgeting focuses on building simple habits first.

For example, if someone earns $4,000 per month after taxes:

- $2,000 goes toward needs

- $1,200 goes toward wants

- $800 goes toward savings or debt payments

This structure makes it easier to balance financial responsibilities while still enjoying life.

Signs You Need a Better Budgeting Method

Here are common warning signs that your current money habits may need improvement:

Beginner-Level Financial Warning Signs

- Running out of money before payday

- Using credit cards for basic expenses

- Missing bill payments

- Having little or no emergency savings

- Feeling stressed about finances regularly

Advanced Financial Warning Signs

- Growing high-interest debt

- Constant overdraft fees

- Low retirement savings

- Poor credit score management

- Impulse spending habits

Benefits of Using a Good Budgeting Method

A proper budgeting system can provide several financial benefits:

- Better control over monthly spending

- Reduced financial stress

- Improved savings habits

- Faster debt repayment

- Better credit management

- More confidence in financial decisions

- Long-term wealth building opportunities

Many beginners notice positive financial changes within a few months of consistent budgeting.

Causes, Financial Risks & Common Budgeting Mistakes

Overspending on Lifestyle Expenses

Many Americans spend heavily on dining out, subscriptions, online shopping, and entertainment without tracking expenses.

Inflation and Rising Living Costs

Housing, groceries, healthcare, and transportation costs continue rising across the USA, making budgeting more important.

Credit Card Debt

Using credit cards without a repayment strategy can quickly lead to high-interest debt.

Lack of Emergency Savings

Unexpected expenses like medical bills or car repairs can create financial hardship without emergency funds.

Common Beginner Budgeting Mistakes

- Setting unrealistic budgets

- Ignoring small daily expenses

- Not tracking subscriptions

- Forgetting annual bills

- Failing to review budgets monthly

- Giving up after one bad month

Best Budgeting Methods Compared

| Budgeting Method | Best For | Pros | Cons |

|---|---|---|---|

| 50/30/20 Rule | Beginners | Simple and flexible | Less detailed |

| Zero-Based Budget | Strict planners | Full expense control | Takes more time |

| Cash Envelope Method | Overspenders | Reduces impulse buying | Less convenient |

| Pay Yourself First | Savers | Encourages saving habits | Less spending control |

| Digital Budgeting Apps | Tech users | Automated tracking | App subscriptions possible |

50/30/20 Budget Rule Explained

The 50/30/20 rule is one of the most beginner-friendly budgeting methods in America.

50% for Needs

These are essential expenses:

- Rent or mortgage

- Utilities

- Insurance

- Groceries

- Transportation

- Minimum debt payments

30% for Wants

These are non-essential lifestyle expenses:

- Streaming services

- Restaurants

- Vacations

- Shopping

- Entertainment

20% for Savings and Debt

This category includes:

- Emergency savings

- Retirement contributions

- Extra debt payments

- Investments

Zero-Based Budgeting Explained

Zero-based budgeting assigns every dollar a specific purpose until income minus expenses equals zero.

Example:

Income: $5,000

- Rent: $1,500

- Food: $500

- Savings: $700

- Debt: $500

- Other expenses: Remaining balance

This method works well for people who want maximum financial control.

Best Financial Strategies for Beginners

Start Tracking Expenses

Before creating a budget, track where your money goes for at least 30 days.

Popular budgeting apps include:

- Mint

- YNAB (You Need A Budget)

- EveryDollar

- Rocket Money

Build an Emergency Fund

Experts often recommend saving at least 3–6 months of essential expenses.

Even saving $500–$1,000 initially can reduce financial stress.

Reduce High-Interest Debt

Paying off high-interest credit card debt can improve financial stability faster than investing early.

Automate Savings

Automatic transfers to savings accounts can improve consistency.

Set Realistic Goals

Examples include:

- Saving for a car

- Paying off debt

- Building retirement savings

- Improving credit score

Smart Money-Saving & Lifestyle Tips

Daily Money Habits

- Track spending daily

- Review bank accounts regularly

- Avoid unnecessary subscriptions

- Cook meals at home more often

- Use cashback or rewards carefully

Financial Mistakes to Avoid

- Ignoring credit card interest

- Taking unnecessary loans

- Overspending during sales

- Relying on “buy now, pay later”

- Not planning for emergencies

Long-Term Wealth Building Habits

- Invest consistently

- Increase retirement contributions gradually

- Improve financial education

- Avoid lifestyle inflation

- Maintain good credit habits

Best Budgeting Apps for Beginners

| App | Best Feature | Ideal For |

| Mint | Free expense tracking | Beginners |

| YNAB | Goal-focused budgeting | Serious planners |

| EveryDollar | Simple budgeting system | Dave Ramsey followers |

| Rocket Money | Subscription tracking | Overspenders |

| PocketGuard | Spending control | Young adults |

When to Seek Professional Financial Advice

Some financial situations may require help from a certified financial professional.

Warning signs include:

- Large debt balances

- Loan defaults

- Bankruptcy concerns

- Retirement confusion

- Tax planning difficulties

- Investment losses

- Financial stress affecting mental health

A licensed financial advisor or credit counselor may help create a long-term plan.

Who Should Care About Budgeting?

1. Students

Budgeting helps manage tuition costs, loans, and limited income.

2. Families

Parents can use budgets to manage housing, groceries, childcare, and savings goals.

3. Office Workers

Budgeting helps balance rising living costs and retirement planning.

4. Freelancers & Gig Workers

Irregular income makes budgeting especially important.

5. Seniors

Retirement budgeting helps manage healthcare and fixed-income expenses.

6. Beginners

Anyone starting their financial journey benefits from learning budgeting basics early.

FAQs

1. What is the easiest budgeting method for beginners?

The 50/30/20 budgeting rule is often considered the easiest because it uses simple percentage categories instead of complicated calculations.

2. How much money should beginners save first?

Many experts recommend saving at least $500–$1,000 initially for emergency expenses before focusing heavily on investing.

3. Are budgeting apps safe to use?

Most reputable budgeting apps use encryption and security features, but users should always choose trusted financial apps.

4. How long does it take for budgeting to work?

Many people notice improved spending habits within 1–3 months of consistent budgeting.

5. Can budgeting improve credit scores?

Yes. Budgeting may help people pay bills on time, reduce debt, and improve overall financial management, which can positively impact credit scores.

Conclusion

Learning what is the best budgeting method for beginners can be the first step toward financial stability and long-term success. For most Americans, the 50/30/20 rule offers a simple and realistic starting point, while zero-based budgeting and digital budgeting apps provide more detailed control.

The key is consistency, not perfection. Small daily financial improvements can create significant long-term results. By tracking expenses, reducing unnecessary spending, building savings, and staying disciplined, beginners can develop healthier financial habits and reduce money-related stress.

Starting a budget today may help create a more secure financial future tomorrow.